REAL ESTATE AGENT JING XUE TELLS YOU THE WHOLE STRATEGY OF BUYING A HOUSE FOR THE FIRST TIME IN THE SAN FRANCISCO BAY AREA!

I believe that for many friends who have just come to work and live in the Bay Area, buying a house here for the first time may be a little overwhelming. Today, Jing is here to talk to you about what you have to know about buying a house for the first time~~

STEP 1: DETERMINE THE GENERAL DIRECTION AND LIST THE BASIC CONDITIONS

- Determine your purchase budget. How much is the down payment? How much can the loan be? Contact a mortgage broker and get a Pre Approval Letter

- Want a school district?

- How many rooms and bathrooms?

- Whether it is a detached house or an apartment, can I accept the property management fee?

- Regarding the loan part, the down payment is not necessarily 20%. It is mainly based on income. Some customers can even make a down payment of 5%. For details, please consult the professional loan brokers of the Jing team.

STEP 2: EVERYDAY ONLINE SEARCH MODE

According to your own general direction, first browse related housing listings on the Internet. Almost all housing listings can be seen online for the first time. Currently, the websites that users use more are: Redfin, Zillow, Realtor, etc.

STEP 3: ON-THE-SPOT INSPECTION

My client friends should hear the most words I say: "It's always better to see more!" Generally, open houses are designed every Saturday and Sunday from 1:00-4:00 pm. Intended home buyers visit. At this time, you need to bring an agent, or you can also inspect the house by yourself, and go to the scene to learn more about the condition of the house.

So at this time, some friends may ask, what do I need to pay attention to on the spot?

- The structure layout is very limited to the structure when viewed online, so the structure can be seen at a glance on site. For those who care about feng shui, you can see which items are taboos in feng shui at this time, such as: whether the door is facing the stairs, whether the house is facing the intersection, etc.

- To the friends who care about the light, please install the compass on your mobile phone, and remember to turn it on when viewing the room! In Greater California, although there is plenty of sunshine all year round, there is still a saying about the orientation. For example, if the window of the room is facing southwest and there is no big tree outside, then in summer, the temperature of the room will be relatively high.

- house status

The bathroom kitchen is a big item in the renovation cost, remember to check the status carefully! Remember to open the cupboard to make sure the inside of the cupboard is in good condition! Check whether there are watermarks on the walls and ceilings, and make sure that there are no water leaks before. If possible, ask the agent present on the water heater, the age of the air-conditioning heater.

Regarding the status of the house, the general seller will provide an inspection report, and the report will have a description of the status of all items, such as: roof age, air conditioner, water heater age, etc.

- Surroundings

If you like all the above items, then at this time, what you need to do is not to leave immediately, but to get in the car, or walk around the house on foot to see the situation of the surrounding neighbors, the environment of the community, etc. Is it easy to park around? Is there a high voltage line? Is there a dumpster? Who are the majority of the people who live there?

STEP 4: LOOK AT HOUSING RELATED DISCLOSURES

In the third step, the above are all the parts that you can see in the house, so the information that you can't see on the surface in many places is all in the disclosures provided by the seller.

Hundreds of thousands of pages of English documents, many buyers do not know where to start. If you don't want to read it, please read the following report carefully.

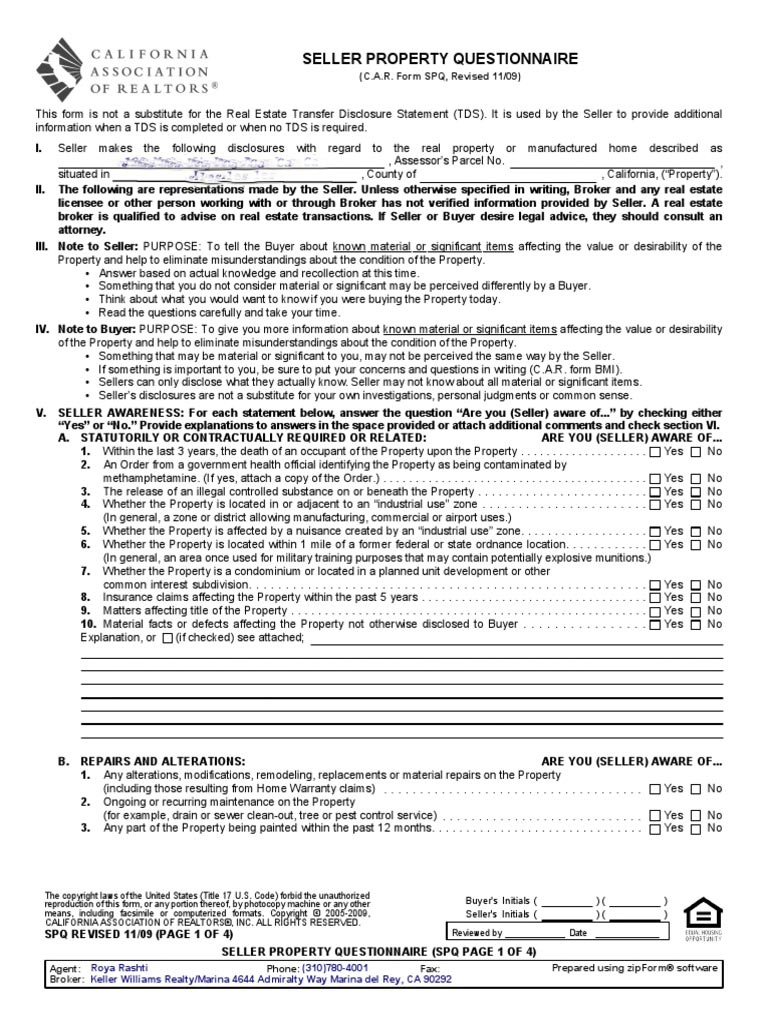

FIRST, LET'S TALK ABOUT THE MAIN ITEMS THAT SHOULD BE PAID ATTENTION TO IN SPQ.

VA1: For those who care about whether someone has died in the house, remember to check the VA1 item in the SPQ provided by the seller. However, the seller will only tell if someone has passed away within three years, and the previous situation has the right not to tell.

VA1: For those who care about whether someone has died in the house, remember to check the VA1 item in the SPQ provided by the seller. However, the seller will only tell if someone has passed away within three years, and the previous situation has the right not to tell.

VA8: In the United States, it is required by law that every home must buy home insurance, and the amount of home insurance will also be related to the number of insurance claims you make. Just like your car insurance. If the seller has claimed too many times in the past five years, it may cause your home insurance cost to double than normal or even make it impossible to buy insurance. Therefore, it is important to review the seller's previous insurance claims before buying a home. If necessary, please ask the seller to provide a CLUE report. If it cannot be provided, you can ask the broker to communicate with the other insurance broker.

LET'S TALK ABOUT THE IMPORTANCE OF TDS (REAL ESTATE TRANSFER DISCLOSURE STATEMENT)

In this document, the amount of information is very large, so be sure to keep your eyes open and look carefully. Generally, for the first-time buyers, I will basically take you to my office to go through these documents, and I cannot come to the office. phone to check one by one.

Here are just two points to keep in mind:

Note 1: Friends who care about whether the seller is renting or owning before look at the black arrow above. Here, the seller is required to  self-help or rental.

self-help or rental.

Note 2: What does the seller leave you? Is there air conditioning and heating? What's in the house? Is the water supply and sewage a normal urban water supply? Is the garage door automatic and how many remote controls are there? Can you take the microwave? Is there an automatic sprinkler system? wait wait wait

For example, the microwave is above, then if the seller removes it when the house is handed over, you can ask your agent to get the microwave version back, or ask for the money from the microwave!

Other projects are not listed here, and friends who have questions are welcome to call me at any time.

ANOTHER REPORT TO NOTE IS THE NATURAL HAZARD REPORT

How do you know if your house is in an earthquake zone? Is your house in the flood zone, the so-called flood zone? Is there any problem with the soil quality around the house? Are there any fuel lines nearby? Are you in a wildfire-prone area?

If some partners think that the possibility of wildfires, earthquakes and floods is too small, don't be afraid. The price is good. That's wrong. It's not that simple. If you are in a fire zone, flood zone, your home insurance will also increase.

WHAT DO WE MAINLY LOOK AT ABOUT THE PRELIM REPORT?

This should be a concern for both realtors and buyers. Generally speaking (except foreclosure auction), a transaction must have title insurance to close escrow. Therefore, there is no need to worry too much about ownership. If there is a problem with the ownership, the title company cannot sell insurance at all, so the transaction cannot end normally.

What else should I pay attention to in the prelim report? Yes, that is the information of easement. The prelim report generally contains easement information. For example, there is a city's electric box on the Lot, which is a part of the easement, and the city has the right to access, and no buildings are allowed on it. This will directly affect the homeowner's addition plan.

Although the vast majority of houses do not have an easement surprise, as a broker and buyer, you must be cautious.

LET'S TALK ABOUT IT NEXT, HOA

Partners who have no community management fee to buy a detached house can skip here directly!

Mention the precautions in the HOA file

- What items are included in property management: facades? roof? Greenbelt? pool? Gym? ?

有没有租房限制?

Some communities have rental restrictions, and the owner occupied ratio varies from community to community. If you are planning to invest, you should pay special attention, even if there is a certain percentage of rental places, you may not know it is the year of the monkey and the month of the horse when you wait in line. Many people have fallen into this pit, only to find out that they can't rent it after buying it

- Is the HOA reserve sufficient, that is, is the reserve sufficient? Is the overall condition of the community good? If the community is in poor condition and the reserve fund is insufficient, the HOA fee will increase. For example, what you can accept now is $300/month, is it acceptable to go up to $380 next year?

其他文件不在这里跟大家一一讲解,但是还有一点可能很多伙伴和经纪人会忽略的项目 ——Property Tax

The configuration of public facilities in each regional government is different, the projects developed in the region are different, and the property tax in each region is also different. Especially for those who buy a new house, they must check the property tax rate before making an offer.

How to check?

Google the county + property tax of your house, and then directly enter the address of the house you want to buy.

Click Look Up Secured Property Tax, and then enter the address.

Make sure all files are complete before proceeding to the next step.

HOME INSPECTION REPORT

In the current market, more and more sellers have completed a house report before the house is listed, and generally provide three basic reports:

In the current market, more and more sellers have completed a house report before the house is listed, and generally provide three basic reports:

General Home Inspection Basic Home Inspection Report

This report examines several major items in the house: plumbing, electrical circuits, air conditioning, heating, hot water system, foundations, etc.

Termite Inspection Report Termite Report

Since the houses in the United States are all wooden structures, it is easy to produce termites, or the wood rots. The termite report will be divided into section 1 items and section 2 items. Section 1 is generally more serious, and it is recommended to repair immediately. The final inspection company will also give an approximate repair price.

Many customers may not dare to buy when they see termites on the report. In fact, it is not so scary. Termites are also very common in California. It depends on the severity. If it is mild, just ask a professional company to deal with it.

Roof Inspection Roof Report

What does the roof report mainly look at? The roof material, the remaining life of the roof, whether there is a repair project, and what is the price.

STEP 5: THE BROKER MAKES AN OFFER

When you see a house that you are satisfied with, the next thing to do is to make an offer! So what information do you need to submit an offer? How to get out?

When submitting an offer, what should a home buyer have on hand?

- Pre Approval Letter from Bank Loan Brokers

- Bank down payment certificate

- Other auxiliary information Jing will add according to the customer's situation before submission. The above is the basic information.

How to make an Offer? How can I get a house at a reasonable price?

This is the time to test your professionalism. If the price is too high, it is a waste of money; if the price is too low, you cannot get a room.

The first step is to analyze the sales data of nearby houses in the past three months, so-called CMA (Comparative Market Analysis). According to the surrounding data, first infer where the normal market price is, and then make corresponding adjustments to the Offer price according to the location and status of the house itself.

In the second step, the market reference data is only the most basic reference step. How much will be the price accepted by the seller in the end depends on the current competition situation, how many people have made offers, and what kind of offers are made? The key! Does the highest price always win?

Here I will tell you that both sellers and sellers’ brokers consider the following two points when choosing multiple offers:

price

Basically, for most customers, the price is their bottom line, and this is often the first point to look at. But this is not absolute.

Terms

How many days does the so-called terms have to complete the transaction, that is, how many days does it take for Close of escrow (COE)? Are there Contingencies? What kind of Contingencies? Contingency is the pre-condition we generally talk about. In the contract, we mention at most three pre-conditions: Appraisal Contingency (up to 17 days), Loan Contingency (up to 21 days) ) and Property Inspection Contingency (up to 17 days). During this protection period, the buyer can withdraw from the contract and get his deposit back on the grounds of these prerequisite clauses. However, for sellers, they don’t want their house to have any variables after entering the contract, withdrawing from the contract, or haggling halfway. Therefore, in the selection of multiple offers, the seller usually chooses the offer with no prerequisites or the least number of days with prerequisites.

For example, Buyer A bids $1 million, but puts a 14-day loan prerequisite, Buyer B bids $990,000, and there is no prerequisite (No Contingency Offer) at all. At this time, the last one who wins the house is often the one who buys the house. home B.

To specify the details of the offer and the detailed description of the Contingency, please call and consult Jing for details.

STEP 6: BANK LOAN

After we get the contract, we usually pay the 3% deposit within three working days. At the same time, the buyer needs to cooperate with the loan broker to start the loan process.

- Appointment Evaluation (Appraisal )

The lender or bank needs to send a special appraiser to the house where the applicant is applying for a loan to conduct a house appraisal. The appraiser knows the contract purchase price, so the general appraisal is basically the contract purchase price. Of course, the price gap between some houses and the surrounding area is too large, which will also cause the appraisal to fail to reach the contract price. At this time, the buyer needs to increase the down payment amount. , or in the case of an appraisal protection clause, the seller is required to reduce the price to the bank assessment price. Bank assessment price is equal to or higher than the contract price, will not have any impact on the loan.

- Lock Rate

Lock Rate, the loan interest rate will fluctuate up and down every day, and the rate will be different in the morning and afternoon. Once the interest rate is locked, it cannot be changed under normal circumstances. During the lock-in period, the interest rate will be guaranteed. Certain lock-in periods range from 5, 10, 15, and 30 years. Generally, the longer the lock time, the higher the interest rate. The so-called 5, 10, 30 years here does not refer to the period during which you have to repay these loans, but the interest rate does not change during this period. For example, if I choose 5 years, the current lock is 2.125, then this 2.125 is only at this interest rate for the next 5 years, and in the 6th year, the interest rate will be adjusted again according to market conditions. Of course, if the market rate is lower than 2.125 over the 5-year term, then refinancing is possible. Generally, banks can refinance the loan after 6 months, please consult the loan broker for details.

- Sign Loan Doc

At the end of the loan transaction, the bank will require the buyer to sign a formal loan agreement and documents. What we call SIGN Loan Document. After the electronic document is signed and arrives at the trading company, the trading company will notify the buyer to go through the final personal signature procedure.

- Bank lending (Funding)

When all the conditions of the lending institution or bank are met, the bank can lend money to the trading company. After the bank's money has reached the trading company, and the buyer's down payment has been received, we can officially take it to the record, and then officially CLOSE!

Here is a summary of some frequently asked questions about loans:

- Q: Is the down payment required to buy a house loan 20% now?A: Not necessarily, the amount of down payment depends on the buyer's income and credit status. If the income status and other conditions are sufficient, the down payment can even be 5%. Please consult your mortgage broker for specific loan amount and down payment amount.

- Q: Pre-approval is issued by Bank A. Can it be changed to Bank B after entering the contract?A: Yes, after entering the contract, the buyer can switch banks, but this process must be completed a few days before the transaction starts, otherwise it will affect the normal completion time of the transaction. I generally remind clients to choose a bank within three days of entering the contract.

- Q: The down payment of the Offer is 20%. After entering the contract, can the down payment ratio be adjusted?A: Yes, as long as the bank can ensure that the adjustment will not affect the completion of the transaction.

- Q: The loan protection clause has been written for 10 days, but the bank's approval result has not been received after 10 days. What should the buyer do?A: As long as the buyer's agent does not submit the Contingency Removal form, the Contingency will be automatically extended. The buyer's agent can also provide the other party with the following Extension of Time Addendum to extend the buyer's protection clause. If the seller does not agree to the extension, or if the buyer fails to submit the Contingency Removal late, a Notice to Perform can be issued to require the buyer to make a decision within a specific time, otherwise the seller can cancel the contract.

- Q: Loan Approved with Conditions, which means that the loan is conditionally approved. Is it safe for me to remove the Loan Contingency at this time?A: Generally, even if we put the loan protection clause, it is usually about 14 days, so it is difficult to achieve loan complete approval within this period. If the loan broker and the buyer have checked the conditions required by the bank It can be added, then the loan protection clause can be removed in this case. Please consult your mortgage broker for details.

STEP 7: TRANSFER THE ACCOUNT OF THE TRADING COMPANY

After the bank has released the loan, the buyer can hand over the rest of the deposit to the trading company, who then gets the County Record. After this step is over, then congratulations! This house is yours! ! The buyer's agent will hand over all the house keys after the record!

Let's think about what is an escrow company? Why do we need such a company to help us complete the transaction when buying a house in the United States? There is a common problem in most real estate transactions: mutual mistrust. As a buyer, would you hand over your hard-earned money to the seller before the condition of the home was up to par? Won't. Likewise, if you are the seller, do you transfer the title to the house before the buyer settles the balance? Also impossible. In the case of mutual distrust, if there is no third party that can eliminate the mutual distrust, the transaction will be suspended. In the process of buying and selling property, even the simplest transactions involve countless details. Like sports games, real estate transactions also need a referee to help buyers and sellers resolve every subtle issue that arises in the process before the transaction is completed.

Escrow is the referee who keeps the game fair. Strictly speaking, Escrow is not on either side of the buyer or seller — they are neutral. They are selfless and impartial third parties to buyers and sellers, and will not have any favoritism. Therefore, during the transaction process, all funds go to the trading company first, and the funds will not be transferred to the seller until the name of the title is changed from the seller to the buyer.

Here, I also summarize some of the questions my clients have asked during closing:

- Q: The house has entered into the contract, but what should I do if my husband is going on a business trip abroad? Is it still possible to transfer normally? A: Yes, in this case, the authorizer needs to sign a Powe of Attorney at the trading company, and authorize his signature to the other party present. That is to say, before the husband goes on business, he can go to the trading company to sign an authorization document and ask his wife to sign it for him.

- Q: The house transaction is completed, why haven't I received the real estate certificate? A: The transfer of property rights in the sale and purchase of houses in the United States is that the owner of the property rights of the house signs a document called grant deed. If you are buying a new house, the developer signs a grant deed document to the buyer, and for a second-hand house transaction, the original homeowner will sign a grant deed document to the buyer. Theoretically speaking, after signing this document, the property right has been transferred from the original property owner to the new property owner. After signing the grant deed, a notarization is required, and then Escrow is responsible for asking the title insurance company to go to the recorder office to register the grant deed and the notarized documents. The day of registration is the day when the transfer is completed, that is, the day when the transaction is closed. The original will be kept in the county, and the transaction company will send a copy to the buyer after the transaction is completed.

- Q: After the transaction is over, I am still worried, how can I check that the house is in my name?A: Method 1: You can go directly to the recorder office of the county registration office with the grant deed to make a payment inquiry. But apart from the property rights company, few people will go to the office to check by themselves. Method 2: You can go to the website of the county tax bureau to check. This method is most commonly used. You can go to the tax website, directly enter the address of a house, and you can see who the owner of the house is. This information is public, which means that you can simply enter the address of a house and see who it belongs to.

Therefore, you don’t have to worry about buying a house in the United States without a real estate certificate. The title deed is the proof of the legal property rights of the house. You can also check it on the US government website at any time. The retrieval of information also saves you from queuing up at the real estate bureau in China and waiting for the clerks to handle all kinds of tedious things. program.

- Q: In the later stage of the transaction, the transaction company sent a form, asking to fill in the property right holding form. How do I choose this? A: For this, I have a detailed explanation and explanation in my public account of real estate information in the San Francisco Bay Area

房子下周就CLOSE了,产权持有方式到底该怎么选?

- Single general choice: A single man / Woman

- If ever married but legally divorced, optional: An unmarried Man / Woman

- If you are married, but you want to own the house by yourself, then choose: A married Man / Woman, as His / Here Sole and Separated Property. Note that in this case, the other party needs to sign a written document agreeing to give up and interest in the property.

- The more common property rights used by husband and wife are: As the Community Property with the right of the Survivorship or As Joint Tenant.

- The general option for multiple people to jointly invest and hold: Tenancy in Common.

Note that in this case, the other party needs to sign a written document agreeing to give up and interest in the property.

Note that in this case, the other party needs to sign a written document agreeing to give up and interest in the property.Please consult the trading company, lawyer or CPA for specific property rights holding methods.